THE COMMERCE PROTOCOL

Belief-Based Ministry Funding, Trust Treasury Administration, and Private Commercial Alignment

Executive Summary

This report examines the Commerce Protocol as an integrated organisational framework that blends (i) a 508(c)(1)(A) belief-based ministry with (ii) a private international trust treasury (commonly referred to as the Asset Fortress Protocol). The Protocol reframes public-facing commerce into belief-aligned private activity, administered through donation → grant → treasury spend flows and governed by orthodox fiduciary principles.

The analysis is descriptive and comparative. It does not assert automatic exemptions or guaranteed outcomes. All effects remain subject to substance-over-form analysis, banking requirements, and applicable law.

1. Commerce, Capacity, and Jurisdiction

Commercial exposure typically arises where activity is conducted by registered legal persons within statutory regimes. The Commerce Protocol addresses this exposure by re-allocating capacity:

• organisational purpose is articulated as a belief-based mission;

• funding is framed as voluntary support (donations) for that mission; and

• financial administration is centralised within a trust treasury acting in fiduciary capacity.

This approach does not deny law or jurisdiction; it aligns activity with capacity.

2. Two-Pillar Architecture

2.1 508(c)(1)(A) Belief-Based Ministry

A 508(c)(1)(A) ministry is recognised under U.S. federal law as a religious organisation. Ecclesia Law research treats “religion” broadly, encompassing sincerely held belief systems with ethical codes, community practice, and mission (e.g., peaceful stewardship; cause no harm; cause no loss).

Within the Commerce Protocol:

• support for the mission is received as donations, not consideration for services; • educational materials, community resources, or programs are framed as mission-aligned benefits, not fee-for-service deliverables;

• split-receipt discipline is applied where a defined benefit has a determinable fair-market value, distinguishing that portion from any voluntary excess.

Outcomes depend on facts, documentation, and conduct.

2.2 Private International Trust Treasury (Asset Fortress Protocol)

The trust treasury is a private international (foreign) grantor trust that:

• operates bank accounts in the name of the trust;

• holds legal title to assets where permitted;

• administers spending and acquisition in fiduciary capacity; and

• remains distinct from grantors, trustees, and beneficiaries, consistent with orthodox trust doctrine.

The trust is not a consumer or trader; it is a fiduciary administrator.

3. Reframing Revenue: Donations and Belief-Aligned Support

Within the Commerce Protocol, revenue is analysed for appropriate characterisation:

• Donations: voluntary contributions to support the ministry’s belief-based mission;

• Mission-Aligned Benefits: materials or access provided consistent with the mission and not conditioned as consideration;

• Documentation Discipline: donor intent, mission statements, and budgets align to support the belief-based framing.

4. Donation → Grant → Treasury Spend

4.1 Ministry Grants

Ministries commonly advance their mission through restricted-purpose grants. Under the Protocol, grants are issued to the trust treasury to fund mission-aligned activities.

4.2 Treasury Administration

The trust treasury:

• pays authorised overheads and operating costs;

• acquires assets pursuant to fiduciary budgets and approvals;

• personal spending.

5. Private Operation and Reporting Context

“Private operation” in research terms means:

• activity conducted through belief-based and fiduciary structures rather than public trading entities;

• public corporate filings are not be triggered where statutory thresholds do not apply;

• bank AML/KYC and beneficial-ownership rules continue to apply to trustees and controlling persons.

6. Abandoned Credit and Treasury Cycling

Ecclesia Law research uses abandoned credit to describe credit value generated by enforceable obligations that is monetised but not reclaimed by the originating party. Within the Commerce Protocol:

• trust spending is a recoupment-qualifying event;

• recovered value is administered by the trust;

• the model is described as spend → recoup → spend.

This framing is descriptive; any recoupment depends on evidence, process, and institutional acceptance.

7. Organisational Efficiency and Risk

Potential efficiency gains include:

• centralised custody and spend;

• reduced duplication across entities;

• alignment of funding with belief-based support;

• conversion of operating costs into accounted treasury activity.

Risks include mischaracterisation, documentation gaps, and substance-over-form challenges. Governance discipline is critical.

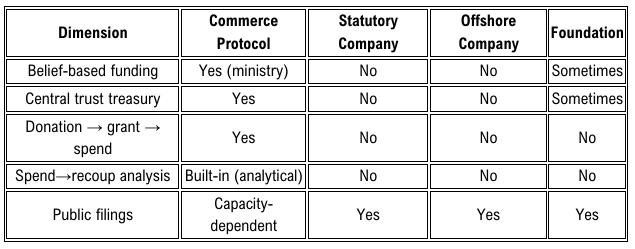

8. Comparative Context

Conclusion

The Commerce Protocol is best understood as a two-pillar, capacity-aligned model integrating belief-based ministry funding with fiduciary trust treasury administration. Its distinguishing feature is the donation → grant → treasury spend architecture, coupled with an analytical abandoned-credit lens applied to treasury operations.

Where properly governed, the Protocol offers a non-adversarial pathway to organise activity privately, administer assets centrally, and evaluate recoupment cycles—without asserting immunity or exemption. Outcomes depend on facts, governance, and acceptance by banks, regulators, and courts applying orthodox principles.